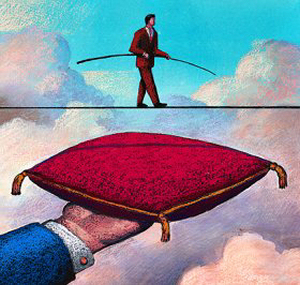

finance & economics, financial crisis, history & society the end of 20th century finance Author The Editor Date January 8, 2009 A eulogy for 20th century finance by one of its greatest poets… The End...

finance & economics, history & society, in other words conspiracy theory Author The Editor Date January 5, 2009 For those still convinced that the Federal Reserve is the lynchpin in some grander...

finance & economics, history & society china inc. Author The Editor Date January 4, 2009 This counter-factual analysis of China’s path toward capitalism reveals that the country’s biggest cities...

finance & economics, financial crisis, history & society, in other words princely finance Author The Editor Date January 2, 2009 This brief history of regal extortion draws some parallels to today’s “sinister” Federal Reserve,...

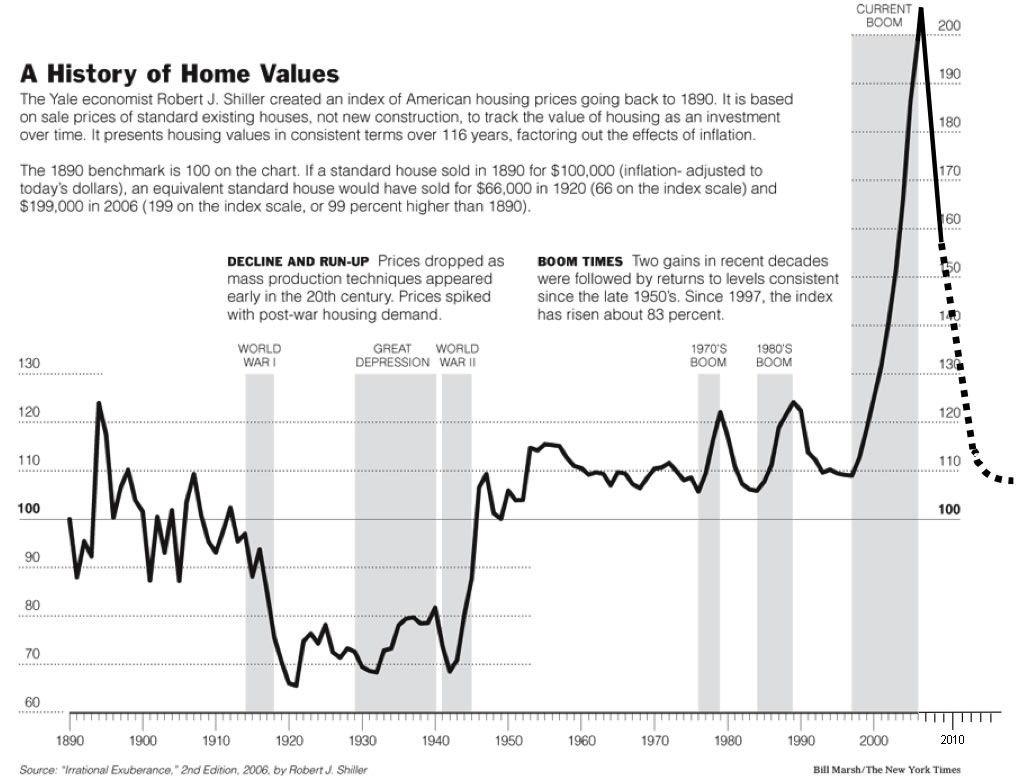

featured, finance & economics, financial crisis, in other words housing freefall Author The Editor Date December 31, 2008 This time series from Robert Shiller puts recent house price fluctuations and their associated...

finance & economics, financial crisis, in other words next shoe to drop Author The Editor Date December 1, 2008 With all eyes on traditional residential mortgages, analysts are now looking for clues in...

featured, finance & economics, financial crisis, in other words the physics of failure Author The Editor Date November 18, 2008 Faith in the underlying mechanics of portfolio theory and market efficiency has certainly contributed...

finance & economics, financial crisis, in other words how to close a hedge fund Author The Editor Date October 21, 2008 Few people will escape from this crisis with enough reputability to scream “I told...

finance & economics, financial crisis, in other words sanity check Author The Editor Date October 11, 2008 Words of cautious wisdom from the celebrated biographer of risk, back in November of...

finance & economics, in other words, world affairs the great black north Author The Editor Date October 3, 2008 As Canadians flock to the polls later this month, quietly supplying 22% of America’s...

finance & economics, financial crisis, in other words the elusive bottom Author The Editor Date September 7, 2008 Even market cheerleaders are struggling to find good news to rally around these days....

finance & economics, in other words the world is fat Author The Editor Date May 28, 2008 Further commentary on the interconnected themes of income disparity, agricultural inflation, and selective de-globalization,...

finance & economics, financial crisis, in other words hot potato Author The Editor Date May 17, 2008 As financial institutions continue to navel gaze in the aftermath of the credit crisis,...

finance & economics, financial crisis, in other words command and control Author The Editor Date May 11, 2008 As markets continue to reel from the too-little-too-late conservative ethos that is snaking its...

finance & economics, history & society, in other words capitalism 2.0 Author The Editor Date March 31, 2008 Social entrepreneurship is at the heart of Capitalism 2.0, and the country’s leading minds...

finance & economics, world affairs speculations on an oil tariff Author The Editor Date March 25, 2008 Assuming that the United States decides to impose a $25 per barrel tariff on...

finance & economics, world affairs question 3 Author The Editor Date February 29, 2008 An excerpt from the mid-term “problem set” in ENR-302… 3. The country of Xanadu...

finance & economics, in other words, world affairs the geopolitics of dope Author The Editor Date February 1, 2008 Another interesting analysis on the trade-off between economics and security. In this case, the...

finance & economics, financial crisis, history & society, world affairs private risk, public reward Author The Editor Date January 18, 2008 An expanded look at the role corporations and hospitable business environments have played in...

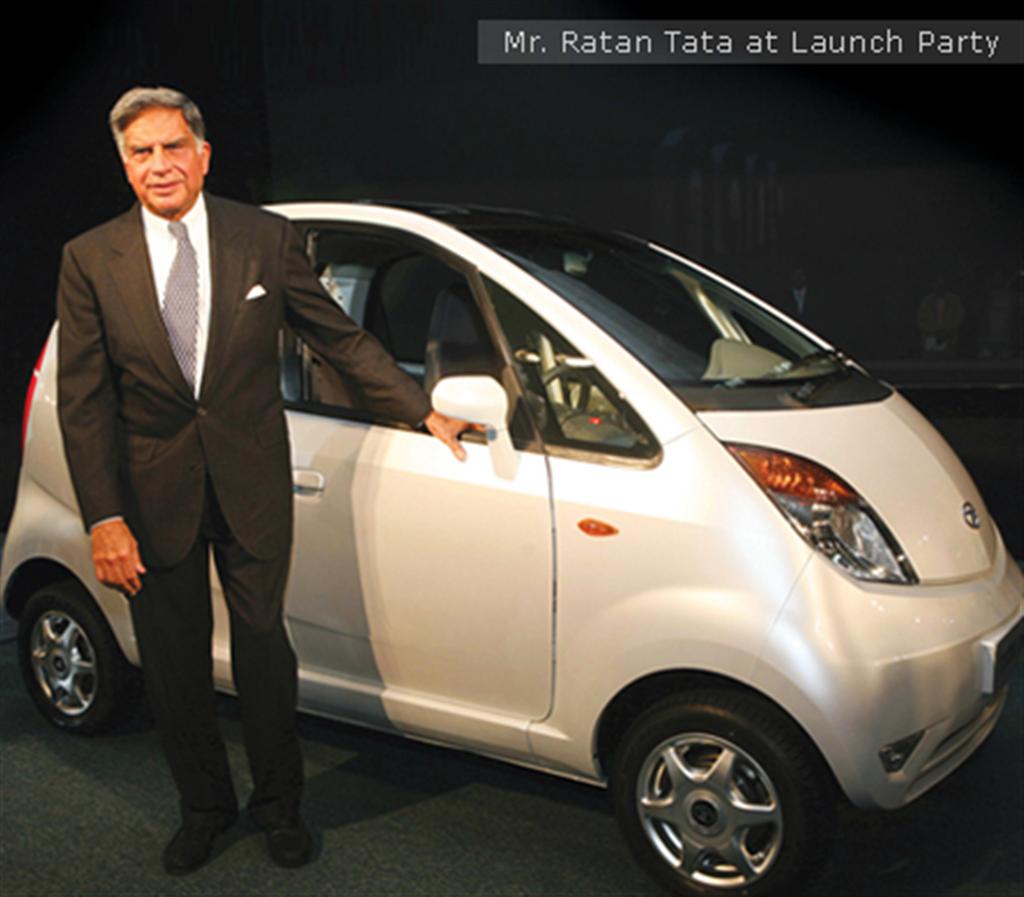

finance & economics, history & society Tata Nano and the Birth of a Middle Class Author The Editor Date January 10, 2008 CAMBRIDGE, MA–It’s been a pretty stellar decade so far in the world’s largest democracy....