Two of the Fed’s greatest leaders and keenest minds have crafted American monetary policy for most of the last three decades, and yet they couldn’t be more different. This is their story.

Two of the Fed’s greatest leaders and keenest minds have crafted American monetary policy for most of the last three decades, and yet they couldn’t be more different. This is their story.

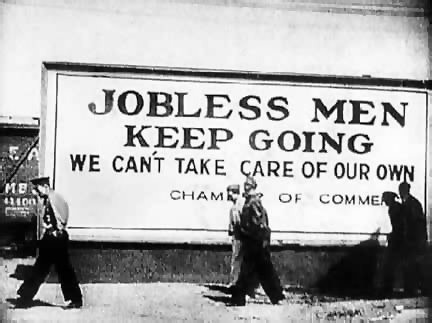

Much like the Great War that preceded it, The Great Depression was never destined to be one-of-a-kind

When Einstein first remarked that “Everything is relative,” he didn’t have Stan O’Neal in mind.

This past weekend was a painful reminder that blood still runs think in humanity’s borderlands.

One could easily mistake this for a modern essay on the virtues of a balanced life and the perils of unbridled greed.

The dogmas of the quiet past are inadequate to the stormy present.

The Blackberry-maker’s biggest failure is not learning from its failures.

The world of finance hails the invention of the wheel over and over again, often in a slightly more unstable version.

A timely and frightening exploration of the causes and consequences of the emerging foreclosure mess.

Students of behavioral finance had a field day this past week.

At issue is an age old debate between two economic philosophies: stimulus as a life vest versus stimulus as a straitjacket.

Evidence continues to mount that established models of rational decision-making are dangerously out of date.

Stopping the spread of financial contagion is deceptively similar to plugging a ruptured deep-sea oil well.

Armies of bulls and bears are camped out on either side of the great debate over the future of the global economy.

Modern politicians, businesspeople and academics are once again questioning both the failures of free markets and the failures of government.

Greenspan casts a surprising shot across the bow of modern banking giants who have grown a little too comfortable with their bailout blanket and artificially low interest rates.

America is just as vulnerable to collapse as the many great civilizations that preceded it — maybe even more so given the increasing complexity of our modern global economy.

A primer on the unique roles that banks and capital markets play in the efficient (and sometimes painfully inefficient) functioning of of modern society.

Zapatero is not a good driver. It’s like a boat, which in calm waters steers fine, but when it gets bumpy, they are not prepared.

It isn’t surprising that so-called “ambulance economics” has gained mass policy appeal as the global economy descends into madness, despite a legacy of failure.

Paul Volcker’s influence is finally starting to resonate where it counts: at both ends of Pennsylvania Avenue.

Over the past generation, a different strain of Christian faith has proliferated—one that promises to make believers rich in the here and now.